August 18, 2025

The Number One Cause of Running Out of Money in Retirement: Sequencing of Returns

By Elliot Palabe, CFP®

Introduction

Retirees often focus on achieving a certain average annual return in their portfolios. However, the sequence of returns – the order in which investment gains and losses occur – can be just as critical. This concept, known as sequence-of-returns risk¹, means that poor market returns early in retirement can dramatically shorten how long your nest egg lasts. Even if your portfolio earns the same average return over the long run, the timing of withdrawals and market declines can lead to very different outcomes for your retirement security.

Understanding sequencing of returns is especially important for those in their mid-50s and beyond, as they prepare to transition from saving to spending their life savings.

What is Sequence-of-Returns Risk?

Sequence-of-returns risk refers to the danger that the timing of withdrawals from a retirement account – combined with market volatility – will negatively impact the portfolio’s overall return and longevity¹.

Once you retire and start drawing from your investments, each withdrawal during a market dip locks in losses. When your portfolio falls in value, withdrawing the same dollar amount requires selling a larger portion of your investments. This accelerates the depletion of your fund and leaves fewer assets invested to grow when the market eventually rebounds².

If that downturn happens later in retirement, the impact is smaller – you’ve already enjoyed growth for many years, and you have fewer years of withdrawals remaining².

Academic research underscores why sequence risk matters so much. A study in the Journal of Financial Planning noted that when a portfolio’s value is eroded by early losses, the fixed withdrawal amount becomes an even larger percentage of the shrunken portfolio, sharply increasing the probability of running out of money³.

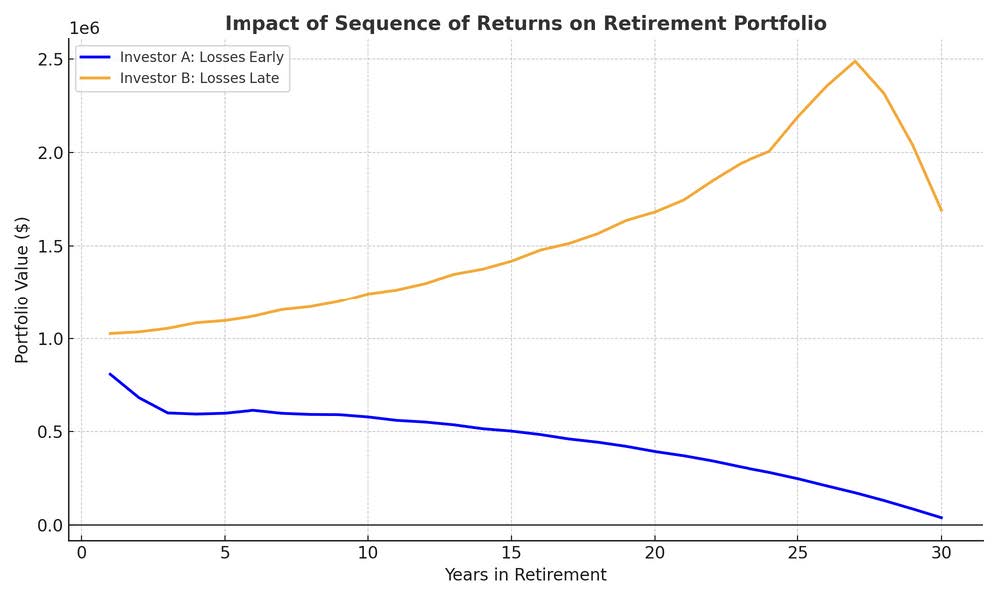

Same Average Return, Different Outcomes: An Illustrative Example

To truly appreciate sequence-of-returns risk, consider a tale of two retirees with identical portfolios:

- Investor A suffers several bad years early on. Losses in the first few years nearly cut the portfolio in half. Later gains arrive too late to fully rescue the portfolio, and the fund is depleted within a couple of decades.

- Investor B enjoys strong early returns and doesn’t encounter the downturns until much later. After 30 years, Investor B’s portfolio is still intact and worth more than double its starting value, despite having the same average annual return as Investor A⁴.

This example shows why the order of returns can matter more than the average return when you’re making withdrawals⁴.

Example:

Initial portfolio value: $1,000,000

Annual withdrawal: $50,000 (taken at the start of each year)

Number of years modeled: 30

Two return sequences:

- Investor A: Negative/low returns in the first few years, positive later.

- Investor B: Same annual returns as Investor A, but in reverse order (good years first, bad years last).

The average annual return for both Investor A and Investor B sequences is about 5.67% per year.

Protecting Your Retirement from Sequence Risk

While you can’t control market timing, you can take steps to reduce the impact of sequencing risk:

- Adjust Your Asset Allocation: Shift to a more conservative mix as retirement approaches to reduce volatility and cushion against downturns².

- Maintain a Cash Reserve: Keep 1–3 years of expenses in low-risk assets to avoid selling investments in a down market².

- Use a Flexible Withdrawal Strategy: Adjust withdrawals based on market performance. Spend less after bad years and allow more in good years².

- Consider Guaranteed Income Products: Annuities or pensions can provide baseline income regardless of market returns.

- Work with a Financial Planner: A professional can stress test your portfolio and design a strategy that anticipates market volatility⁵.

What Does This Mean for You?

Sequence-of-returns risk highlights the fact that timing can be everything. For those nearing retirement (or newly retired), it’s crucial to recognize this risk and plan for it.

This reality highlights the importance of working with a financial professional as you transition into retirement. An experienced advisor can help you develop a withdrawal strategy that prepares for market volatility and protects your income for the long haul.

As always, Palabe Wealth is here to help. If you’re unsure how sequence-of-returns risk might affect your retirement, let’s discuss it together. Schedule a 15-minute introductory phone call by contacting us directly at (847) 249-6600.

References

- Investopedia – Sequence Risk: Meaning, Retirement, and Protection, Julia Kagan, updated May 20, 2025.

- Charles Schwab – Timing Matters: Understanding Sequence-of-Returns Risk, Rob Williams, Nov 7, 2023.

- Frank, Larry R. Sr. & Blanchett, David M. – The Dynamic Implications of Sequence Risk on a Distribution Portfolio, Journal of Financial Planning, June 2010.

- Kiplinger – Don’t Let Sequence of Returns Risk Cook Your Goose, Ted Thatcher, Sept 17, 2024.

- Western Carolina University – New study on ‘4% rule’ suggests different approaches to retirement strategies, Dec 12, 2023.

Elliot Palabe, CFP®

Elliot Palabe is a Wealth Advisor at Palabe Wealth, where he plays a pivotal role in designing comprehensive retirement plans and working directly with clients to address their financial needs. Elliot's expertise lies in his ability to combine personalized Financial Planning with strategic Tax Planning, helping to ensure that each client's financial strategy is both optimized and aligned with their individual goals and circumstances.

Elliot has a solid educational foundation that underpins his professional acumen, as he holds a Bachelor’s degree in Finance from the Foster College of Business at Bradley University. His academic background has provided him with a deep understanding of financial markets, investment strategies, and economic principles.

Elliot is a CERTIFIED FINANCIAL PLANNER™ professional. He holds several critical financial industry licenses, including the Series 65, 63, 6, and SIE, held through LPL Financial. These qualifications enable him to offer comprehensive investment guidance and demonstrate his thorough knowledge of the financial services industry.

A specialist in the use of sophisticated financial planning and tax planning software, Elliot brings a technological edge to his approach. This expertise allows him to create detailed and highly personalized financial plans that can adapt to changing market conditions and tax environments. By leveraging cutting-edge technology, Elliot ensures that Palabe Wealth's clients receive the most accurate, up-to-date, and effective financial advice possible.

His work is instrumental in helping clients navigate the complexities of financial planning and retirement preparation, helping to ensure they are well-positioned to pursue their long-term financial objectives.

Outside of work, Elliot competes in pickleball. The game’s blend of strategy and precision reflects the same qualities he brings to financial advising - thoughtful planning, attention to detail, and focus.